For all your real estate needs in California... Specializing in beach properties on the coast, the Westside, Silicon Beach and greater LA.

My website: www.sandralew.kw.com

Email: sandy.lew.broker@gmail.com

Cell: 310-963-1623 CalBRE#01920376

Keller Williams Realty South Bay

23670 Hawthorne Blvd

Torrance, CA 90505

Great news for LA's silicon beach. In 2016 the city's startups have received around $3 billion in funding. LA has become the third most prominent place for startups in America following behind San Francisco and New York. We have the great weather, good universities, a relaxed beach lifestyle, large pool of talent and lower costs compared to SF and NY. For now, all eyes are on "Snapchat" in Venice to continue to thrive and go public to help further establish LA as an enduring place for startups.

Besides my passion of real estate I really love to travel. I've been to

over 36 countries in the past 9 years along with all over the states.

The social aspect is what I love most about real estate. I tend to agree

with this article as Spain, Dubai and the United Kingdom are my other top favorite places

to live besides Silicon Beach in LA! I grew up in SF bay area's Silicon Valley as well

so very familiar with all these global hot spots. Which is your favorite? I'd love to connect with others and continue making friends all around the globe. Let me know how I may help you with your real estate needs.

by Virginia Harrison @vharrisoncnn September 15, 2015: 10:06 AM ET

San Francisco is named one of the strongest markets for international property investors.

It's time to buy American homes.

The U.S. has been named the

hottest market for global residential property in a survey of 14

countries by real estate advisors Savills. The researchers analyzed

economic and demographic trends to forecast how much prices in popular

cities will rise over the next five years.

And the essential ingredients for solid returns? A combination of population growth, rising wealth and limited housing supply.

1. United States

The U.S. housing market has enjoyed three years of growth as the economic recovery gathers pace. Prices are up about 30% from their 2009 trough.

San Francisco offers

the most impressive growth potential. Nearby Silicon Valley has spurred

interest in the city and secured its place as one of the country's best

performing housing markets. Savills named it ahead of New York, Los

Angeles and Miami.

But tread carefully. Savills director Yolande Barnes said there's a

huge gulf in potential between the tech hotspots and rustbelt cities.

As for who's buying, Canadians are the top foreign purchasers of U.S.

property by sales, followed by buyers from Mexico, India and the U.K.

2. United Arab Emirates

Wealth creation and positive demographics underpin the scope for solid

returns in Middle East property. The Gulf economy has clocked annual

growth of at least 4% for the past three years.

Dubai is the

region's major real estate hub, and Savills believe its long-term

prospects are supported by the city's role as a global business center. Dubai skyline. 3. Singapore

Measures to cool the overheated Asian market, coupled with a general

slowing of the economy, has slugged sales and reduced prices in

Singapore's prime residential market.

That could be good news for keen investors, however, because underlying demand remains strong, Savills said.

4. United Kingdom

Two European countries round out the top 5 -- Britain and Spain. The dynamics differ but both economies are strengthening and benefit from low interest rates.

Prices in London's residential market

are enjoying a massive boom -- up 9% over the past year alone -- but

demand overall remains buoyant, and the supply of new homes tight. Look

for opportunities around the burgeoning tech sector in the capital,

Savills said.

London property prices have surged in recent years, far outstripping price growth in the rest of the U.K.

5. Spain

Teetering on the brink of collapse in 2012, the Spanish economy has turned its fortunes around to become one of Europe's standout performers this year. Real estate prices in the country are still more than 25% below their 2008 peaks, but the market has stabilized.

Property investors should consider Spain's Balearic islands, such as

Majorca and Ibiza, Savills said. Popular with European tourists, these

residential markets have been more resilient than those on the mainland,

thanks to a diverse demand base and limited new supply. The island of Ibiza is one of Spain's more promising real estate markets for investors.

Realtor.com predicts an uptick translating to around 40% for first time home buyers for the Spring 2017 season. Based on web analysis of searches they make up 52% of prospective buyers. With nearly half of the recent strong job growths created in the 24 to 34 years old range it may translate to them finally being able to afford the down payment to make the plunge to purchase their first home. With mortgage lenders offering more first time home buyers incentives with lower downpayments it may make buying a viable option over renting.

First-Time Buyers Expected to Return to Housing Market

Realtor.com data shows rise in web searches by house hunters who want to buy in 2017

By Laura Kusisto

Young buyers could return to the housing market in droves this spring, according to a report due to be released Wednesday.

First-time

home buyers now make up 52% of prospective buyers looking to purchase

in 2017, up from 33% a year earlier, according to an analysis of web

searches performed by Realtor.com, a real-estate listing website.

Buyers

typically begin searching several months in advance, so the jump in

activity could translate to increased purchases by first-timers in the

spring and summer of next year.

‘The first-time buyer is ready to come back.’

—Jonathan Smoke

The absence of first-time buyers has been one of the biggest

abnormalities of the housing market in recent years. If they return, it

could provide a big boost to sales and serve as a sign that the housing

market is returning to normal after years during which most new

households being formed were apartment-dwellers.

“The first-time buyer is ready to come back,” said Jonathan Smoke, chief economist for Realtor.com.

Just

because many more young people are searching for homes doesn’t mean

they will be able to buy.

A number of surveys have shown that

millennials want to purchase homes but are being held back by their

inability to save for a down payment as well as a general lack of

affordable inventory and strict mortgage-lending standards.

Nonetheless, Mr. Smoke said he anticipates the share of first-time

buyers could rise to 40% during the peak 2017 selling season. First-time

buyers fell to 32% of all purchasers in 2015, the lowest level in three

decades, according to the National Association of Realtors.

Historically, young buyers have averaged 40% of all home buyers,

according to the group.

News Corp, owner of The Wall Street Journal, also operates Realtor.com under license from the National Association of Realtors.

Strong

job growth could be one major reason more young people are looking to

buy homes. Nearly half of the new jobs created in the past year were

filled by people ages 25 to 34 years old, the prime age for buying a

first home, according to Mr. Smoke. Mortgage lenders have rolled out

more programs allowing first-time buyers to purchase homes with lower

down payments.

Nonetheless,

some big obstacles remain. Chief among them: Builders are still

constructing few homes affordable to younger buyers and inventory of

existing starter homes remains tight.

Ultra-wealthy still interested in buying real estate despite slowdown, uncertainty

International investors desire investing in the United States real estate market. Surveys show that nearly 25 percent of the global top 1 percent in the United States expect to purchase new property compared with a whopping 45 percent of the global top 1 percent of the international buyers over the next three years. While homes in the higher end selling for over $1 milion based on surveys in 12 countries markets are somewhat slowing overall but hot pockets are still sizzling. With elections soon approaching consumers remain cautious yet optimistic.

Javier E. David | @TeflonGeek

Sunday, 23 Oct 2016 | 4:50 PM ET

Despite the chill winds of a softening luxury real estate market

and political uncertainty across the globe, it's still a buyer's market

for the ultra-wealthy, a recent survey suggests.

In partnership with the

YouGov Affluent Perspective, Luxury Portfolio International surveyed the

top echelon of consumers across 12 countries, finding that the majority

of those consumers were "cautious but optimistic" in the face of an

uncertain and often turbulent world economy.

To be sure, the ranks of the

ultra-wealthy, those with more than $50 million or more in net worth,

have swelled. Research from Credit Suisse showed that there are more

than 123,000 individuals in this category, a whopping 53 percent jump in

just five years. Most of them reside in North America, where the rate

of growth among the super-rich is double that of Asia and significantly

faster than Europe's.

Although high-end real estate has softened — sales of homes priced above $1 million have tumbled recently, according to recent National Association of Realtors (NAR) figures

— high-net worth individuals "feel good about their lives, are

confident about their decisions and have a very strong intent to

purchase real estate," the report's authors wrote.

As such, real estate is still in demand for the economic elite, but varied somewhat depending on their location.

The YouGov survey found that

25 percent of the wealthy were looking to purchase new property over the

next three years, with 18 percent looking to sell. Outside the U.S.,

the mood was far more confident: 45 percent of wealthy buyers are

looking to purchase real estate with only 23 percent looking to sell,

the data showed.

The report showed that

"nearly 1 in 4 of the Global Top 1 percent plans to make a real estate

purchase in the next three years, with almost as many considering

selling as well."

The YouGov survey is consistent with what Philip White, president and CEO of Sotheby's International Realty Affiliates, told CNBC in an interview last month.

He said high-end real estate was "sort of a mixed bag, and obviously

there is some slowing," but some locations were faring better than

others.

Huge new mixed use development breaking ground in early 2018. The entire area around the expo has positive improvements with the dedicated bike lanes and now is getting more user friendly for pedestrians and connecting it to transit—namely,

the Expo Line’s Expo/Bundy station a block away

What’s next for West LA’s big new development Martin Expo Town Center?

A new grocery store, offices, restaurants, and more than 500 apartments coming to Olympic and Bundy

By

Bianca Barragan

Sep 30, 2016, 9:44a

A big Westside project, the Martin Expo Town Center, won

unanimous approval from the Los Angeles City Council last week, a

decision that will usher in new retail, residential, and a 10-story

office tower on the site of a car dealership at the northwest corner of

Olympic Boulevard and Bundy Drive.

The project has been tweaked and trimmed since we last saw it

at the beginning of the year. The most notable reductions are on the

retail and office front. Office space was shaved down from 200,000

square feet down to 150,000, and the grocery store, once 50,000 square

feet, has been slimmed down to 35,000 square feet. (The project also

includes 18,000 square feet of restaurant space and 46,000 square feet

for general retail use.)

The town center has also gained a few significant

add-ons, namely an affordable housing component that will set aside 20

percent of the project’s 516 apartments for less-than-market rate rents.

(Fifteen percent will be "workforce housing," where occupants median

income can't exceed 150 percent of the area median income, and five

percent will be for very low-income tenants.)

The project has also acquired a lot of upgrades geared at

making it friendly for pedestrians and connecting it to transit—namely,

the Expo Line’s Expo/Bundy station a block away. In addition to

widened, 15-foot sidewalks, the new complex will have a half-acre

pedestrian plaza, as well as a smaller, 4,000-square-foot

pedestrian-oriented area at the corner of Olympic and Bundy, acting as a

sort of staging area for people heading over to the light rail station,

project manager Phil Simmons tells Curbed. There will also be 100

short-term and 600 long-term bike parking spots, as well as bike

storage. There are also more than 1,500 underground car parking spaces.

"We think we’ve got as close to a perfect TOD [transit-oriented development] as possible," Simmons said.

The new mixed-user is being developed by the Martin

family, which for over 40 years has owned and operated a Cadillac/GMC

dealership on the site. (Two dealership-related buildings on the site

would be demolished to make way for the new development.) Simmons says

the Martin family’s long presence in the neighborhood helped garner

support from locals.

But not everyone was swayed. Last month, the West Los Angeles Neighborhood Council told the

City Council the project would, "make our community a more dangerous

place to live." The letter cited "significant traffic impacts" as the

main reason for the neighborhood group’s opposition.

Now that plans are approved, the next step for developers

is to prepare "working drawings." Simmons said he expects it will be

"close to a year" before they apply for building permits. Developers aim

to break ground in early 2018.

The very hot silicon beach housing market has resulted from growing high tech firms in the area. Wow! Did you know that 86 percent of the nearly 700 tech firms in LA are located in Silicon Beach according to CBRE? No wonder there has been such a demand in housing. People want quality of life and desire to live close to where they work. Great jobs, coastal breezes, upscale shopping, hip restaurants, gyms, and proximity to the beach lifestyle make here worth every penny.

I've personally experienced so many multiple offers for my buyers. It's the lifestyle and potential upside with more dense conservative ratio of employees to work space that drives greater housing needs as well. Housing supply has not kept up with demand thus driving up prices and rents.

Silicon Beach keeps on scaling upward and outward

Rents soar in hot hoods, but expansion could prove to be a market equalizer

September 22, 2016 10:30AM

From the L.A. print issue: In

less than a decade, Silicon Beach has grown from a Silicon Valley

outpost in Santa Monica to encompass a stretch of coastline as far south

as Playa Vista and as far east as Culver City. Market pros are now

closely watching whether the high-tech enclave will continue marching

south to El Segundo, eating up real estate along the way.

Fully 86 percent of the nearly 700 tech

firms in Los Angeles are located in Silicon Beach, according to CBRE.

The roster includes such boldfaced names as Facebook, Google, Hulu and

Snapchat, as well as high-tech incubators and startups — such as

DogVacay and Scopely — which haven’t (yet) achieved household-name

status.

But experts say this isn’t a replay of

the dot-com bubble in the late 1990s, when startups rushed to get big in

order to score an initial public offering while the market was red hot.

These days, brokers say, young tech companies aren’t land-banking

office space, as they did back then.

“You don’t see 50 employees taking 20,000

square feet,” said Jaclyn Ward, an associate at JLL’s Los Angeles

office. “They’re being pretty conservative.”

This tendency, in turn, has kept the

sublease market fairly tight and given landlords pricing power in the

core market in Santa Monica. Sublease space is more plentiful on the

periphery, in Playa Vista.

“The challenge in Silicon Beach is a

pretty continual lack of space that pushes rental rates up,” said George

Pino, the co-founder and CEO of Commercial Brokers International.

However, he added, the continued expansion of Silicon Beach into new

neighborhoods could become an equalizing force on market prices.

Here’s a look at some of the biggest deals and most notable tenants in the area’s key beachheads.

Santa Monica

In downtown Santa Monica, where tech

firms vie fiercely for prime locations, vacancy rates hover in the

single digits and asking rents have soared to $7 or $8 a square foot per

month, up from an average of $4.61 just a few years ago, according to

data from JLL. But in outlying areas, some big-name companies have

pulled up stakes. Both Yahoo and The Honest Company have decamped for

Playa Vista, leaving tens of thousands of square feet in their wake.

In the second quarter of 2016, Santa

Monica overall had a 17 percent office vacancy rate and average asking

rents of $5.40 a square foot, according to JLL. Ward said the “massive

exodus” for Playa Vista in 2015 and early 2016 led to the higher vacancy

rates, although some of that space has already been absorbed.

In early 2016, Oracle inked a deal to

expand from 80,000 square feet to approximately 130,000 square feet in

The Water Garden, located at 1620 26th Street. The building is currently

being renovated to include collaborative work space in its lobby and an

outdoor seating area with a fire pit, said Michael Nieman, an attorney

in private practice who is also a commercial real estate broker at CBRE,

and who represents the building.

In June, AwesomenessTV, a teen-targeted

video-streaming company majority owned by DreamWorks Animation, closed

on a 90,000-square-foot lease for its headquarters at Pen Factory, a

Clarion Partners property at 2701 Olympic Boulevard.

Venice

Venice Beach has some of the highest

asking rents in Silicon Beach, with prime space renting for upward of $8

a square foot. Google is a large tenant, with a 100,000-square-foot

campus environment in three buildings, including the historic Binoculars

Building designed by Frank Gehry. In front of the building is a giant

binocular-shaped sculpture by Claes Oldenburg and Coosje van Bruggen.

Snapchat is another key tech player in

the area. In 2015, the company doubled the size of its Venice Beach

lease at the intersection of Venice and Abbot Kinney boulevards to

40,000 square feet. In 2016, it leased 80,000 square feet in city-owned

structures at the Santa Monica Airport, including two buildings and

eight hangars. Snapchat has agreed to make $1.4 million in improvements

to the buildings for a rent credit of five months.

“Snapchat is always a hot topic,” Ward

said. Founded in a beachfront bungalow on Ocean Front Walk in Venice

Beach in 2011, the company later moved into roomier quarters at 63

Market Street, also in Venice Beach. It continued to expand by inking

more leases around Venice Boulevard.

Playa Vista

Playa Vista certainly isn’t playing Kmart

to Santa Monica’s Target, but many market pros do see it as a veritable

bargain. With average asking rents below $5 a square foot and a wealth

of new creative space, Playa Vista — just minutes south of Santa Monica —

has attracted new and established tech companies alike. At least 80

percent of Playa Vista’s commercial space is occupied by technology,

entertainment and media companies, including many industry heavyweights,

such as Facebook, Microsoft, YouTube, IMAX and Sony Playstation.

The Silicon Beach stronghold has even

been immortalized on TV. Scenes for ABC’s “Revenge” were filmed at the

Water’s Edge office complex, located at 5510 Lincoln Boulevard, which

includes a reflection pool and recreation areas. Electronic Arts leases

nearly 150,000 square feet in two buildings, and sublets space for

filming at Water’s Edge.

In 2014, Google spent $120 million to buy

12 acres next to Howard Hughes’ famed “Spruce Goose” airplane hangar,

which is zoned for nearly 900,000 square feet of commercial space. Then,

in 2016, the company acquired a long-term lease for the hangar as well.

YouTube, a Google subsidiary, has

occupied space next door since 2012, when it became one of the first

tenants in the newly opened Hercules office campus, which also occupies

land formerly owned by the Hughes Aircraft Company. Dubbed “YouTube

Space LA,” it’s a spot where YouTube video creators — either employees

or people from outside the company — can collaborate.

In April 2016, Facebook scooped up a

long-term lease to a three-story, 55,000-square-foot building being

developed by Vantage Property at the east end of the Playa Jefferson

office campus. The project is slated for completion in late 2017, and

Facebook will occupy 35,000 square feet of the building, said Jonathan

Larsen, a principal and managing director of Avison Young in Los

Angeles.

In the summer of 2016, Yahoo was also preparing to move

from space it has long occupied in Santa Monica, into a

130,000-square-foot space in the new

Collective campus on Playa Vista’s West Bluff Creek Drive.

The Honest Company, an organic

personal-care products retailer founded by actress Jessica Alba, moved

its headquarters here in 2016, taking an 83,000-square-foot spread

across the top three floors of the i|o building, which is located at

12130 Millennium Drive. The fast-growing startup had revenue growth of

more than $150 million in 2014 — the most recent year for which the

private company has released data.

Culver City and El Segundo

Unlike other areas in Silicon Beach,

Culver City’s asking rents are holding the line. The average rate for

Class A office space remained flat, at $3.33 a square foot, during the

first half of 2016. This makes rents here substantially lower than in

other areas of Silicon Beach, where year-over-year increases of 50 to 75

percent are not uncommon.

Culver City has around 800,000 square

feet of vacant office space, according to JLL. But brokers say that

soaring prices in popular coastal neighborhoods such as Venice Beach

have spurred bargain hunting here that might absorb some of the

inventory.

WeWork, which operates co-working office

space in markets from Los Angeles to New York, signed a long-term lease

for 75,400 square feet at 5782 Jefferson Boulevard in Culver City in

April 2016. The company plans to move in by late 2016, despite slashing

its profit forecast by nearly 80 percent in July.

Farther to the south, El Segundo is being

eyed as the next expansion area for Silicon Beach. The neighborhood

already has multi-family buildings and office space, albeit much of it

is in need of renovation.

“In Silicon Beach, some companies start

with one person and some start with five, but they exponentially grow

and add space,” Larsen said. “The next Honest Company is out there,

growing, below the radar.”

Real estate is getting it's own sector in the S&P 500. Very important impact on real estate investment trusts as they move into a different category and out of the financial sector. Huge impacts on the financials as it had included them. Good time to re-balance and take a look at your investments.

Investors moving billions into real estate ahead of a big market change

September 8, 2016 - CNBC

Real estate stocks are getting a place of their own in the market this week, and investors are taking notice.

As of the close of trading Friday, the industry will become its own sector in the S&P 500 (^GSPC), bringing the broad market index up to 11 divisions .

The move primarily affects real estate investment trusts (REITs),

moving 28 issues with nearly $600 billion in market cap out of the

financial sector and into the new real estate heading.

The

decision came primarily because officials at S&P Dow Jones Indices

believe the industry has become large enough that it should be split

from the broader financials that include commercial and investment

banks, insurers, brokerages and exchanges.

Practically speaking, there's an important impact on investors.

Portfolios

that track the S&P 500 will have to be readjusted to accommodate

the new sector, which is expected to account for just over 3 percent of

the total index. Financials, which currently account for about 13.1

percent of the S&P 500, likely will drop below 12 percent.

That means investors looking to achieve balance in their portfolios will have to adjust their allocations accordingly.

Ahead

of the move, investors have been piling money into real estate funds.

In fact, the sector has generated the largest inflows to exchange-traded

funds this year of any of its peers, pulling in $1.08 billion in August

alone and $7.6 billion for 2016, according to figures released Thursday

by State Street Global Advisors.

Among individual funds, the biggest gainer by far has been the $35.7 billion Vanguard REIT Index Fund (NYSE Arca: VNQ), which has pulled in $4.57 billion this year. The $2.87 billion Schwab U.S. REIT (NYSE Arca: SCHH) ETF has collected $706.2 million, while the $4.3 billion iShares Cohen & Steers REIT (NYSE Arca: ICF) fund has had inflows of $355.2 million. (All numbers according to FactSet.)

Investors

in the sector have been rewarded. The Vanguard fund is up 12.6 percent

year to date, nearly doubling the 6.7 percent that the S&P 500 has

returned.

S&P

chose Friday to introduce the real estate sector because the day also

marks a "triple witching" in the market. The term refers to the

expiration of contracts for stock index options, index futures and

options during the final hour of trading.

That will give market participants time to reallocate on a day where conditions are conducive to making changes.

"It's

a day with a huge amount of liquidity in the market, trading is faster

and more efficient than usual, and it's a good day for people to

rebalance their portfolios," said

David

Blitzer, managing director and chairman of the index committee at

S&P Dow Jones Indices.

"There will be some people who will be

rebalancing their portfolios to make sure their weight in real estate is

the right weight."

The

sector is part of the Global Industry Classification Standard

implemented in 1999 to help investors make sure they could see what was

moving the market and make decisions accordingly.

In a nutshell these 6 charts help to visualize the major impact housing has on our economy.

These 6 Charts Tell You Everything You Need to Know About the Real Estate Market

By Chris Matthews

The housing market has done a lot of healing, but it also has a long way to go.

There’s likely no sector as important to the U.S. economy as housing.

In the first quarter of 2016, residential investment accounted for

roughly half of the 1.1% increase in real GDP. Historically, this is on

the high side, but when you count spending on housing services as well

as spending on various kinds of housing construction, the home

construction industry can account for as much as one fifth of overall

output in the U.S. economy.

That’s why housing has traditionally powered the American economy out

of recessions, and that’s why housing’s role as the trigger of the

Great Recession was so damning to the subsequent recovery.

While housing

prices have improved—with home values in some markets higher than

before the crisis—there’s evidence that the housing bust has inflicted

long-term damage on the home building industry and therefore the

American economy. Here are 6 charts from Torsten Slok, Deutsche Bank’s

Chief International Economist, that show the state of the housing market

and how it’s powering, and holding back, the rest of the economy.

People Really Want to Buy Homes

There’s evidence that the millennial generation has been slow to warm

to the idea of homeownership, as they are generally delaying decisions

like marriage and child rearing. But as this chart shows, overall,

Americans are still in the market for new homes.

But Homebuilders Have Been Slow to Respond to Demand

The rate at which homebuilders are constructing new single family

homes remains quite depressed, despite steadily increasing demand. Those

in the business have argued that supply-side factors, like increased regulation and a short supply of skilled labor as reasons they have been slow to meet demand.

The Homes Being Built are Mostly for the High End of the Market

There are many metrics that one can use to show that homebuilders

have decided that it makes sense for them to target wealthier buyers,

but the above chart is striking. During an otherwise sluggish economic

recovery, the increase in the size of new homes for sale has actually

accelerated.

Because Middle-Class Homebuyers Can’t Get Financing

Home builders aren’t the only business that has been turning it’s

back on the American middle, for the simple reason that middle class

incomes have been on the decline for years now. Furthermore, the

mortgage finance industry is still leery of lending to all but the most

creditworthy borrowers.

Rental Markets are Tighter Than They’ve Been in Generations

The lack of credit available for new homebuyers has forced more and

more homeowners into the rental market, driving up rents and put further

pressure on already strained middle-class budgets.

Hope springs eternal.

Despite what appears to be a negative feedback loop of stagnating

middle-class incomes, tight credit, and a homebuilding industry that

can’t profitably cater to most of the country, demographics have

analysts hopeful that things will turn around in the future. The modal

age in America is 26, and this echo-boom generation has yet to settle

down and seriously consider homeownership. Analysts hope that this new

demographic wave will jolt the housing sector back into pre-bubble

normalcy. And we’re moving in the right direction.

Time heals all wounds, even in the real estate market.

Why home prices in Southern California keep climbing

Real estate is a hot commodity these days especially in Southern California. It boils down to the pent up demand and lack of inventory, scarcity of land to build, continued low mortgage interest rates and improving job outlook. All these factors play into the surging home prices with no let up in sight especially as markets reach or even surpass their previous historical peaks.

The Southern California housing market is red-hot again.

By James F Peltz - July 14, 2016

Home

prices in the region have been climbing steadily, as they have

nationwide, toward record levels not seen since the 2008 housing crisis

plunged the country into a severe recession.

The S&P/Case-Shiller home price index, a widely followed gauge of

the market, showed that prices in the Los Angeles market in April stood

at their highest point since October 2007.

The median home price

in Orange County in May was $651,500, surpassing its bubble-era peak

reached in 2007, according to the real estate data firm CoreLogic.

Interest rates of about 3.5% or less for 30-year, fixed-rate mortgages — not far off the all-time low of 3.31% in November 2012 — have helped fuel the gains.

Dana

Kuhn is a lecturer at the Corky McMillin Center for Real Estate at San

Diego State University, and we asked him to summarize the market and

what it means for would-be buyers and sellers. Here’s an edited excerpt:

Has the Southern California housing market completely recovered from the recession?

In

the most desirable markets, that’s essentially true. That would be West

Coast large-metro areas. The San Francisco Bay Area is now priced above

its peak numbers of the last decade. Orange County, too, and Los

Angeles and San Diego are getting very close to their former peaks.

Seattle is doing really well. Portland is doing well.

One of the worst-hit areas in the housing crisis was the Inland Empire. How is that region faring?

That

was the real subprime [mortgage] disaster area. Those markets have been

slower to recover. There are areas like the Inland Empire that are

probably only between 80% and 85% of [their pre-bubble] peak.

Is it surprising that it’s taken this long?

Yes and no. Given how severe the recession was, there was so little

production [of new housing] in that time. There was a four-year period

between September 2008 and September 2012 when the nation’s housing

starts were below all previous troughs going back some 40 years. And in

those previous troughs, what you typically had was one year at that

nadir, and then you’d climb back up fairly quickly. But we had four

years below all of those troughs, and so production obviously fell

behind demand.

So there was a huge pent-up demand when people

started getting jobs and believing in housing again. The industry has

struggled to keep up with it in the more desirable markets.

Is that driving the surge in prices?

Yes.

Like most things, it’s a supply/demand situation. The number of

[housing] starts hasn’t been able to take care of that pent-up demand.

The pricing has gone up accordingly, and that has been accommodated by

low [mortgage] interest rates. Continued low interest rates have in

essence subsidized a rapid ascent in pricing.

Why is it tough to add more housing to the supply in Southern California?

Land

is increasingly scarce, and that’s forcing people to build up rather

than out. And those higher-density projects are more sensitive

politically, more difficult to get approved and take longer to get

through the pipeline. You can have agreement about needing more housing

in a given market, but when it actually comes down to [building] those

300 units on that corner in that neighborhood, you get resistance. So it

can take years in Southern California coastal areas to get [those]

projects approved. That’s true whether it’s a for-sale product or a

rental market.

This all sounds good for sellers, but is it a tough time to be a buyer?

Yes. Unfortunately real [inflation-adjusted] wage growth hasn’t kept

up with that surge in pricing. It’s significantly harder to buy

something now than it was a few years ago because people’s wages just

haven’t kept up, even though interest rates are still the same.

The median price of a house in Los Angeles County is above a half-million dollars. How does a first-time buyer afford that?

They

don’t buy that house. That’s the middle of a statistical group. Your

first-time buyer is pretty much forced to buy a [less-expensive]

attached product, not detached.

Like a condominium?

Yes. And they’re probably

not going to be able to afford to buy that unit in the same neighborhood

in which they would rent if they were renters. So they have to make a

lifestyle concession in order to become homeowners.

Meaning they would build up equity in that house, then later sell it in hopes of buying one in the neighborhood they desire?

Right.

Also, the millennial generation [18 to 34 years old] has eschewed the

concept of home ownership because they saw their parents and others get

burned in the last downturn and because they prefer lifestyle over

ownership.

But as they get older and have kids they’ll have a

different outlook. And as their wages increase, they’re also going to

realize the importance of the mortgage deduction — the tax benefits that come from home ownership — and there will be move back toward home ownership.

Do you see prices continuing to climb?

The peak value in any given cycle has always exceeded the peak value in the previous cycle. So there was no question in my mind — even during the depths of the downturn — that

we would get back to peak [price levels] because we always have. It’s

only a question of how long it takes to get there. Of course it took

quite a long time this time because [the recession] was so bad.

The only question is how many more years of increases beyond that peak can you expect? I don’t know anyone who can tell us that.

While the dollar volume of sales decreased, number of homes purchased actually increased most likely due to the changing demand for locations of homes.While previous international buyers have mainly purchased in expensive locales they are now expanding to less expensive areas as well. Chinese buyers still rank the highest investors followed by Canadian buyers. Given today's volatility in global financial markets, real estate is still one

of the safest investments available.

Foreign buyers flood US real estate, but buy cheaper homes

Diana Olick - 7 hours ago

Chinese investors negotiate at the US-China Real Estate summit & trade fair in Beijing. (File photo).

The appetite for U.S. real estate continues to

flourish, but international buyers are shifting their sights from luxury

to less-pricey properties. This may be due to overall higher home

prices, along with a stronger U.S. dollar, which both cost foreign

buyers more at the negotiating table. There are also fewer nonresident

foreigners investing in the market.

"Weaker economic growth throughout

the world, devalued foreign currencies and financial market turbulence

combined to present significant challenges for foreign buyers over the

past year," said Lawrence Yun, chief economist of the National

Association of Realtors (NAR). "While these obstacles led to a cool down

in sales from nonresident foreign buyers, the purchases by recent

immigrant foreigners rose, resulting in the overall sales dollar volume

still being the second highest since 2009."

Foreign buyers purchased $102.6 billion of

residential property in the U.S. between April 2015 and March 2016,

according to NAR's annual report on international activity in U.S. real

estate. That is a 1.3 percent decline in dollar volume from the previous

survey. The number of properties purchased, however, rose 2.8 percent

to 214,885. The value of homes bought by foreigners was typically higher

than the median price of all U.S. homes.

"The slight drop in dollar volume

can probably be accounted for based on the types of properties

purchased, and the locations of many of those properties. We've seen at

least some evidence that foreign buyers — both investors and people just

looking for a home — have begun looking beyond expensive markets like

San Francisco, New York City and Washington D.C., and buying properties

in smaller, less-expensive cities in the Southeast and Midwest," said

Rick Sharga, executive vice president at Ten-X (formerly Auction.com),

an online real estate marketplace .

Another major shift was in the

makeup of international buyers. Chinese purchasers continued to outpace

all others, with their dollar volume exceeding the total of the next

four ranked countries combined. Their dollar volume of sales, at $27.3

billion, was a slight decrease from last year's survey but was still

three times as much as Canadian buyers, who were ranked second. Chinese

buyers also bought the most expensive homes at a median price of

$542,084.

"Although China's currency

modestly weakened versus the U.S. dollar in the past year, it's much

stronger than it was five to 10 years ago, thereby making U.S.

properties still appear reasonably affordable over a longer time span,"

wrote Yun in the report.

Given today's volatility in global

financial markets, real estate is one of the safest investments

available. U.S. real estate in particular is relatively inexpensive

compared to properties in Asia.

"The explosive growth of the

Chinese economy created a very large number of very wealthy people.

As

that country's economy has slowed down, those individuals are looking

for better investment alternatives, and many have concluded that U.S.

real estate is a smart bet," added Sharga.

London had been a favorite of

foreign investors, but the impact of the Brexit vote is already hitting

the housing market there. Buyers from the United Kingdom were the

fourth-largest consumer of U.S. real estate in the data that was

gathered before the Brexit vote.

"Sales activity from U.K. buyers could very well

subside over the next year depending on how severe the economic fallout

is from Britain's decision to leave the European Union," added Yun.

"However, with economic instability and political turmoil outside of the

U.S. likely to persist, the world view of American real estate as a

safe investment should keep demand firm even as pressures from a

stronger dollar continue to weigh down on affordability."

As for U.S. destinations, five

states accounted for half of foreign buyer purchases: Florida, (22

percent), California (15 percent), Texas (10 percent), Arizona and New

York (each at 4 percent). Latin Americans, Europeans and Canadians, who

historically favor warmer climates, were most prevalent in Florida and

Arizona. Asian buyers flocked to California and New York. Texas was more

a mix of buyers from Latin American, the Caribbean and Asia. Texas may

be more of an investment play, as demand for single-family rentals there

remains strong.

Sales to nonresident foreign

buyers fell to the lowest dollar volume since 2013. Shares to foreign

residents increased. The shares had been evenly split, but higher home

prices and the depreciating value of foreign currencies likely played

into that dynamic.

"Led by Venezuela (45 percent) and

Brazil (24 percent), at least eight countries, including China and

Canada, saw double-digit percent increases in the median sales price of a

U.S. existing home when measured in their country's currency," added

Yun.

The Brexit vote has directly impacted interest rates in the United States. This summer is a good time to shop for a home mortgage as analysts are predicting rates may drop even further. Good opportunity for those who are home shopping, looking at real estate as an investment or looking to refinance their existing home loans.

Brexit could prove advantageous for borrowers in real estate market

Posted: Friday, July 1, 2016 12:00 amBy RHETT MORGAN

World Staff Writer

Married and a father of four children, including a newborn, Tulsa’s Mike Guillen was seeking ways to save money. A refinancing opportunity gave him one.

Guillen

this week secured a 15-year, fixed-rate of 2.87 percent on his home

near 101st Street and South Memorial Drive, a drop of more than one

point from his previous rate.

“It was just too good of a deal to pass up,” said Guillen, who works for a local heat-and-air company. “I was floored.”

He purchased his family’s 3,300-square-foot home about seven months ago.

“After

looking at the math — because I was going to do the house pay-down

account — I’m going to come out more ahead by having a low interest rate

than I would have by putting the money in the bank and trying to earn

on it,” Guillen said.

In

the wake of the United Kingdom’s decision to leave the European Union,

stories such as Guillen’s could become increasingly more common.

The move, also known as Brexit, has some analysts predicting that rates could drop even further.

“The

latest statistic I saw is that we are in a three-year low of interest

rates again,” said Ed Adams, who leads the retail mortgage channel for

Tulsa-based BOK Financial Mortgage.

“We

continue to be in a place where there are historically low interest

rates, which presents a real good opportunity for buyers who are

thinking about home ownership or refinancing or move-up opportunities or

real estate as an investment.”

Thirty-year, fixed-rate mortgages have been hovering in the 3.5-percent range, he said.

“People

still believe you need a 20-percent down payment to buy a home when you

look at national surveys,” Adams said. “The truth is, there is a lot

more opportunity. There’s a lot more product available to help with low

down payment-type loans and options to get into home ownership.

“The

continued pressure to keep interest rates down and what recently

happened with Brexit is certainly providing opportunity for people to

think about real estate as an asset and a part of their total net

worth.”

Bankrate.com,

which puts out a weekly mortgage rate trend index, found that almost

half of the experts it surveyed believe rates will remain relatively

unchanged in the coming week while a third believe they will fall

further.

According to the latest data released Thursday by Freddie Mac,

the 30-year fixed-rate average plunged to 3.48 percent with an average

0.5 point. (Points are fees paid to a lender equal to 1 percent of the

loan amount.) It was 3.56 percent a week ago and 4.08 percent a year

ago.

Since

the beginning of the year, the 30-year fixed rate has plummeted nearly

50 basis points. (A basis point is 0.01 percentage point.) It has fallen

18 basis points in the past month alone.

The

15-year fixed-rate average sank to 2.78 percent with an average 0.4

point. It was 2.83 percent a week ago and 3.24 percent a year ago.

The

five-year adjustable rate average dropped to 2.70 percent with an

average 0.5 point. It was 2.74 percent a week ago and 2.99 percent a

year ago.

“In

the wake of the Brexit vote, the yield on the 10-year U.S. Treasury

bond plummeted 24 basis points,” Sean Becketti, Freddie Mac chief

economist, said in a statement. “This week’s survey rate is the lowest

since May 2013 and only 17 basis points above the all-time low recorded

in November 2012. This extremely low mortgage rate should support solid

home sales and refinancing volume this summer.”

Developer plans to break ground soon on redevelopment of Pier 44.

More changes coming to Marina Del Rey in area dubbed Silicon Beach. Looks like developers got the green light to go ahead with the development of a new shopping destination which includes a Trader Joes with seaside dining as well as a boat dock along with waterfront restaurants and retail. There will also be a wide pedestrian walk that will also be bike friendly.

Posted June 16, 2016 by The Argonaut in News

By Gary Walker

The California Coastal Commission has rejected an appeal against the

redevelopment of Pier 44 in Marina del Rey, allowing construction of new

restaurants and retail — including a waterside Trader Joe’s specialty

grocery story — to break ground along Admiralty Way as early as this

year.

Santa Monica-based developer Pacific Marine Ventures LLC plans to

reconfigure the boat sales, maintenance and dry dock facility into an

83,253-square-foot shopping and dining destination encompassing eight

new structures.

In addition to a Trader Joe’s with a seaside dining patio, parking

for boats and a water taxi stop, the new Pier 44 would set aside another

8,000 square feet for waterfront restaurants and include a public

pedestrian promenade along the waterfront that’s 28 feet wide. A new

location for boating supplies retailer West Marina and a new home for

the South Corinthian Yacht Club are also in the mix, with space for 462

cars and 100 bicycles to park.

The Coastal Commission June 9 vote to reject the appeal was unanimous.

Jon Nahhas, a frequent critic of Marina del Rey development who

founded the small boater advocacy group the Boating Coalition, had filed

the appeal against Pier 44’s coastal development permit.

“Marina del Rey was built for the recreational enjoyment by the

residents of Los Angeles County. It was not built for the residents as a

destination to shop. Based on the information available, it appears

that the approved project is inconsistent with the [coastal development]

policies related to traffic, public participation in the

decision-making process, public access, non-water related uses in the

tidal zone and the overall policies of the California Coastal Act,”

Nahhas wrote in his appeal.

Nahhas also complained that the new Trader Joe’s location does not

provide adequate parking and that not enough was being done to mitigate

local traffic impacts. He also charged that officials did not allow for

adequate public participation in the review and permitting process, a

frequently voiced concern about new development in Marina del Rey.

The project has been approved by Regional Planning and the

supervisors. Nahhas was appealing a decision by the supervisors, who

turned down his initial appeal of the planning commission’s approval.

Aaron Clark, a land-use consultant with Armbruster Goldsmith &

Delvac LLP who is representing Pacific Marine Ventures, characterized

Nahhas and his Boating Coalition as a “coalition of two.”

“The appellant’s chief allegation is that the project will adversely

impact the public’s ability to access the coast, in contravention to the

Coastal Act’s access policies. We categorically reject that false

allegation,” Clark wrote to the commission about the appeal.

Now that the project can move forward, Clark said Pacific Ventures would try to obtain building permits as quickly as possible.

“We’d anticipate breaking ground by late summer or fall,” he said.

People are influenced by their networks (the company they keep- friends/relatives/co-workers) and not just by their neighborhoods. FOMO - the fear of missing out comes into play when they see the positive affects being a homeowner has with people around them. It's a direct influence as people tend to mirror those closest to them. This motivates them to buy to have a successful investment in the housing market. Facebook friends matter. Do you want to rent or own? Simple interesting facts.

Is FOMO Driving Your Housing Decisions?

People who are favoriting their friends’ smart housing purchases are more likely to make their own.

Kriston Capps - May 24, 2016

Fear of missing out may be a more powerful force than any of us

realize. According to a new study, FOMO—or something like it—may have a

direct influence on how people make decisions in the housing market. And

that influence appears to be profound enough to affect housing prices

at the county level.

A new paper released by the National Bureau of Economic Research

finds a link between a person’s Facebook network and her housing

investments. The paper shows that people whose friends have positive

experiences in the housing market are more likely to buy themselves.

They’re also more likely to buy a larger home, more likely to pay more

for a home, and more likely to make a bigger down payment when their

friends are making successful investments.

The work—assembled by Facebook economist Michael Bailey, Harvard

University’s Ruiqing Cao, and Johannes Stroebel and Theresa Kuchler of

New York University’s Stern School of Business—combines Facebook survey

data with public-record information on housing transactions. Starting

with a broad and diverse market of users in Los Angeles County, the

researchers examined how their geographically distant networks, which

usually amounted to people situated in just a few discrete areas,

affected their investment decisions.

We first analyze 1,242 responses to a housing market survey among Los

Angeles-based Facebook users. Over half of the survey respondents

report to regularly talk to their friends about investing in the housing

market. The survey also asked respondents to assess the attractiveness

of property investments in their own zip code relative to other

financial investments. Holding respondent characteristics fixed, we find

a strong relationship between the recent house price movements in

counties where a respondent has friends, and whether that respondent

believes that local property is a good investment.

Now, it would only make sense that a person would take her neighbor’s

experience in the housing market as instructive advice. A person who

talks to her friends about their experiences with

investments is doing crucial research. But this research seeks to

determine “the plausibly-exogenous variation in the recent house price

experiences of an individual’s geographically-distant friends as

shifters of her local housing market expectations.”

Meaning, the way that a L.A. resident’s friends’ housing-investment

experiences in, say, Oklahoma City influence her decisions about her own

perspective on L.A. So the researchers factored for recent transplants

and other factors that might influence how much L.A. residents might

weigh their social networks versus local networks.

“We find that the house price experiences within an individual’s

social network have quantitatively large effects on all four aspects of

her housing investment decision,” the paper reads. Those four aspects

are:

Extensive margin decision (rent or own)

Intensive margin decision (size of the home)

Willingness to pay for a particular house

Leverage used to finance the purchase (down payment)

According to the paper, people whose friends experience a 5

percent increase in house price over a 2-year period (from 2008 to 2010)

were 3.1 percent more likely to buy a house within the next 2 years

(from 2010 to 2012). This is a pronounced effect—more than half the size

of the effect of adding another member to the household (such as a

spouse).

Further, people with friends who were getting the most out of the

housing market—in this case, a 5 percent increase over a 2-year

period—were paying more for their own homes (3.3 percent) and making

larger down payments (7 percent). This effect on a person’s own market

decisions is correlated to a person’s cumulative social-network

experience, including geographically distant networks.

The researchers also found the inverse to be true: When a person’s

social network had experienced negative outcomes in the housing market,

she was less likely to transition from renter to homeowner status or

take other risks in the market.

“We argue that the relationship between the house price experiences

in an individual’s social network and her housing market behavior is due

to the effects of social interactions on her housing market

expectations,” the paper reads—suggesting that liking or favoriting a

friend’s upward mobility could plausibly make a person more likely to

invest in the housing market. The effect is more pronounced for more

social individuals:

For respondents who report that they regularly talk to their friends

about whether property is a good investment, we find a strong

relationship between their friends’ house price experiences and their

own assessment whether property in their own zip code is a good

investment. Indeed, for respondents that often talk to their friends

about property investments, the effect size is twice the effect size of

the average individual. For respondents that never talk to their friends

about investing in the housing market, no statistically significant

relationship is found.

This paper might help to explain how housing shocks are contagious

across geographic boundaries. When it comes to investment decisions,

people pay attention to their networks, not just their neighborhoods.

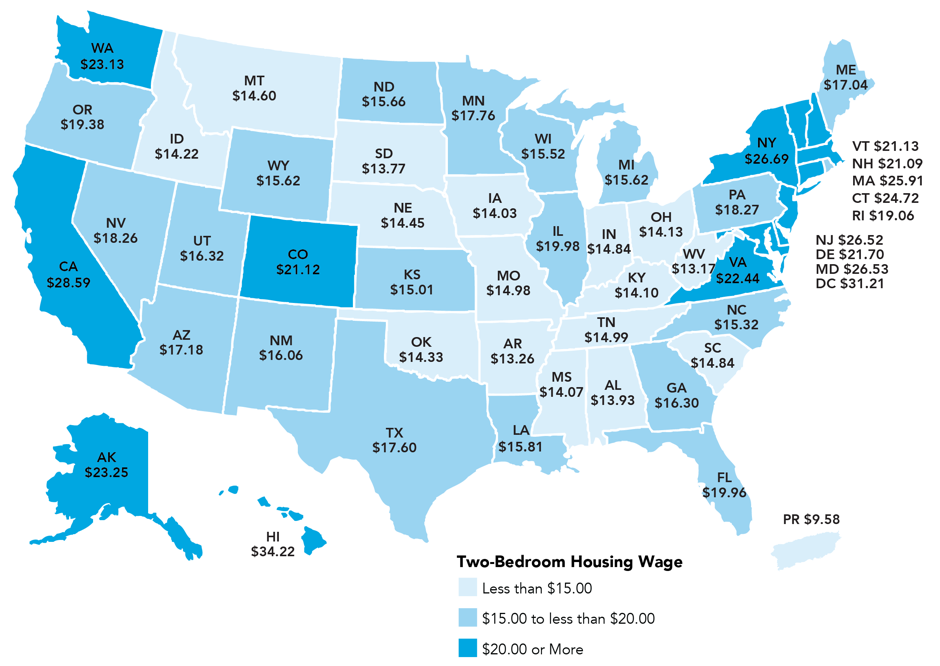

Skyrocketing demand for affordable rentals continues as the average wage earner struggles to be able to afford to live in some of the priciest states. In 2016, a worker would need to make at least $20.30/an hour to rent a simple basic two bedroom home without devoting more than 30% to housing costs. Of course, this varies by city and states but it's definitely an eye opener.

The Hourly Wage Needed to Rent a 2-Bedroom Apartment Is Rising

A new report maps how much the average American has to earn to comfortably afford a modest rental in every U.S. state.

By Tanvi Misra - May 26, 2016

In 2015, the demand for rental apartments reached its highest level ever since the 1960s. The pinched access to mortgage credit after the Great Recession is one reason why. Anotheris that many Americans—especially the poor and people of color—haven’t felt the effects of theeconomic recovery, and may not be able to rustle up the funds for a down payment. A third reason is that Millennials, now the largest generation ever since the baby boomers, are especially loath to buy homes. The supply of rentals, especially at the lower end of the market, has been no match for the skyrocketing demand.

That means it’s getting harder and harder for average Americans to afford a modest rental in the U.S., a new report

by the National Low Income Housing Coalition finds. “The lowest-income

renters without housing assistance have always struggled to afford

housing, but in recent years they have become even more squeezed as more

households enter the rental market,” Andrew Aurand, the vice president

of research at NLIHC, tells CityLab.

In 2016, a worker would need to make $20.30 per hour to rent a

two-bedroom accommodation comfortably—without devoting more than 30

percent of income on housing costs. Last year, NLIHC pegged this

“housing wage” at $19.35 an hour.

(And we’re not talking about luxury apartments here. The report tallies

this average hourly wage against the Department of Housing and Urban

Development’s Fair Market Rent, an annual estimate of what a family might pay to live in a simple apartment.)

To really understand the weight of 2016’s housing wage, consider

this: The average hourly wage for Americans is actually $15.42 per the

report, which is not nearly enough to afford a two-bedroom. And the

federal minimum wage, at $7.25, is around a third of what’s required.

That means minimum-wage workers would have to work three jobs, or 112

hours a week, to be able to afford a decent two-bedroom accommodation.

From the report:

If this worker slept for eight hours per night, he or she would have

no remaining time during the week for anything other than working and

sleeping.

Of course, both the rental-housing market and hourly wages vary by

state. The map below illustrates the differences in “housing wages” by

state. Among the states, Hawaii has the highest hourly wage requirement

($34.22) for a two-bedroom. Among U.S. metros, San Francisco is at the

top with $44.02.

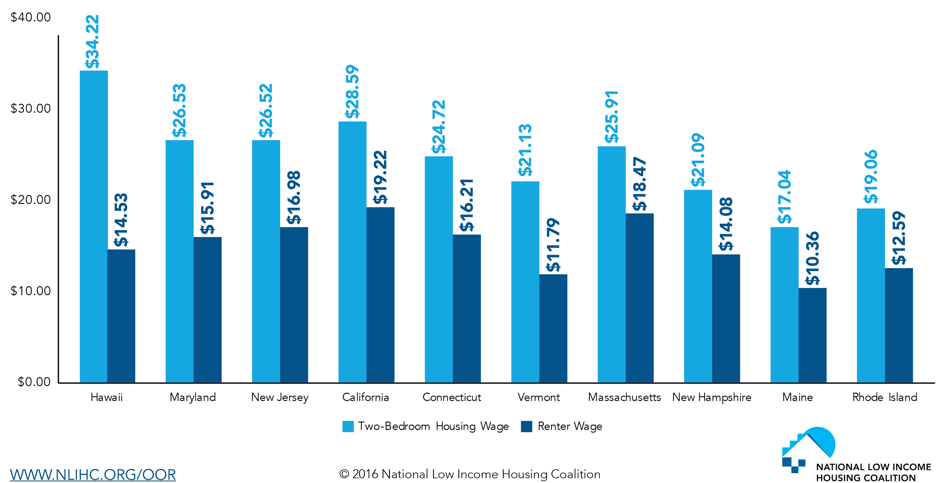

And here’s a graph showing the states with the biggest gaps between

the current hourly wages and housing wages. Again, Hawaii leads this

list: For

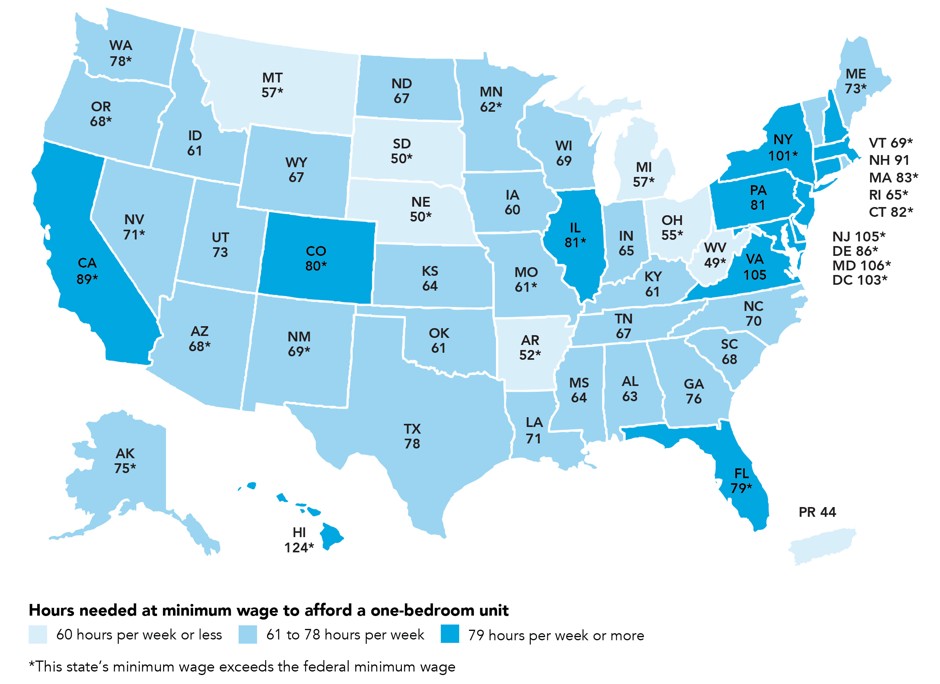

poor Americans, even a one-bedroom place is out of reach. There’s not a

single state in the U.S. where a minimum-wage worker can comfortably

afford a one-bedroom by working a 40-hour week. The map below shows the

hours per week this worker would have to put in live in a modest

one-bedroom in each state:

Raising the minimum wage would undoubtedly narrow these gaps, but it’s still just not enough:

“At least 22 local jurisdictions now have a minimum wage higher than

their prevailing state or federal level. All fall short of the

one-bedroom and two bedroom Housing Wage,” the report reads. The key

lies—you guessed it—in expanding the affordable housing supply. Writes

HUD Secretary Julian Castro, in the report’s preface:

This report confirms that investing in affordable housing — as HUD is

doing by providing annual housing support for nearly 5.5 million

households and through the new national Housing Trust Fund, as part of

innovative efforts like the Rental Assistance Demonstration, and with

incentives like the Low Income Housing Tax Credit — is one of the most

important steps we can take to help people succeed today, and live

healthier lives long into the future.

The Share of $1 Million–Plus Homes in L.A. Has Doubled (MAP)

LA Home prices still going up... it's gone insane the past four years. As a realtor, with multiple offers still a reality in this price range its a matter of supply and demand. For now, it's still a sellers market. Volume of sales has slowed but I think it's due to lack of inventory. Yikes!

By Dennis Romero - May 19, 2016

If you're looking for evidence that L.A.'s real estate market has gone absolutely insane, look no further.

A

new report from real estate listings site Trulia titled "Million Dollar

Creep" says the Los Angeles market's share of million-dollar homes has

more than doubled between 2012 and 2016.

In some neighborhoods, residences worth $1 million or more often outnumber those worth less, the site found.

"In

certain neighborhoods in Los Angeles, the contrast is especially

striking — in Mar Vista, the share of million-dollar homes jumped from

22.4 percent in 2012 to 74.1 percent in 2016," a Trulia spokeswoman

said. "In Silver Lake, the percentage share grew from 7.8 percent to

just under one-half of homes valued at a million dollars or more (43.8

percent)."

Otherwise the L.A. areas with the highest increases in $1 million–plus

homes over the last four years were in the South Bay (Torrance), near

Beverly Hills (South Carthay) and in Glendale, according to Trulia.

"Each of the major Southern California housing markets — Los Angeles,

Orange County, Ventura County, and San Diego — have witnessed a

doubling in the share of million-dollar homes over the past few years,"

the site said in a statement.

Nationally, L.A. ranked fifth for markets with the largest percentage increases in million-dollar homes from 2012 to 2016.

The Bay Area's San Francisco, San Jose and Oakland took the three top

spots, respectively, Trulia found. Orange County was fourth nationally.

San Diego was seventh. And Ventura County was ninth.

Trulia says it looked at home values, not just listings, in 100 of the nation's largest metro areas.

Check

out the map below. If you're shopping for a home in L.A. right now,

you're either technically rich or very optimistic. In either case, good

luck.

We have the most sophisticated and wealthiest generation of baby boomers thus far. Traditional stereotypes of retirement are out the window. Large percentage of today's baby boomers are an urban savvy group of Americans. A quality lifestyle that affords mental stimulation. They want to live in the same places as the younger generation where the cool people hang out. Amenities, modern day conveniences, walkable cities, proximity to restaurants, galleries, concierge services, as it's their time to really enjoy the carefree lifestyle.

Reverse Migration: How Baby Boomers Are Transforming City Living

By Clare Trapasso

It’s the traditional migratory circle of life: Young folks flock to

the blazingly bright cities to make their careers and have their kicks;

middle-aged peeps move to the burbs, buy homes, and raise their broods;

older Americans search out warmer, cheaper, and more

water-aerobic-centric climes to make their retirement nests. End of

story, right? But hold on. Baby boomers have changed just about

everything over the past few decades. Now, as more enter their twilight

years, they’re changing the face of American cities, too.

Instead of migrating south en masse to retirement

communities in the Sunshine State or the wilds of Arizona, more and more

baby boomers—a particularly urban-savvy group of Americans—are moving

back to the metro areas they abandoned when they began raising families.

And in leaving their suburban homesteads, these empty nesters are

redefining the urban centers they now call home. Again.

Boomers, defined as those born between 1946 and 1964, are the

largest and wealthiest generation to ever retire—a fact hardly lost on

savvy developers and businesses. Larger and more expensive city

residences chock-full of active senior–friendly amenities, like

round-the-clock concierge services, are going up across the country, And

more upscale, boomer-targeted shops and restaurants are opening their

doors to serve these newly minted urban dwellers.

The numbers are beginning to tell the tale. Only 11% of buyers aged

50 to 59 closed on homes in urban areas and central cities from July

2013 through June 2014, according to a 2015 National Association of Realtors® report. A year later, that percentage had edged up to 13%. At first glance it doesn’t seem to be an overwhelming leap, but when you consider that there are an estimated 74.9 million boomers, even a minority can make an impact.

And it seems that the bigger the city, the bigger the appeal. “If you

can afford to live in Manhattan, it’s a great place to be older,” says Jonathan Smoke, realtor.com®‘s

chief economist. “You’re not shoveling snow. You can walk or get

transportation to any doctor or service you need. And you have a

friendly doorman that pays attention to you and acts as an additional

caretaker.”

The influx of the older and wiser is particularly pronounced in the

most walkable cities and lots of college towns, Smoke says. These areas

tend to be full of condos as well as restaurants, shops, and cultural

venues such as museums and theaters. They also often have classes and

workshops that are popular with retirees. They’re packed with cool

places, cool things to see, cool people. And scarcely a shuffleboard

court to be found.

“The interesting trend is that the places where many young people

want to live are the same places where many retirees want to live,”

Smoke says.

Sick of the suburbs

Many of New York City real estate agent Victoria Woolley Parry‘s

clients are former urbanites who are moving back because they don’t

want to spend their golden years maintaining a big house in the boonies.

And they crave the mental stimulation found in the City That Never

Sleeps.

“It’s a lot of work to live in the suburbs,” says Parry, a

Manhattan agent with Parry Properties of Keller Williams. They’re

“looking to shed themselves from the suburban entanglements of having to

care for the pool or the lawn or getting strangled by the ivy.”

Most of her older clients are wealthy suburbanites buying condos and co-ops starting at $1 million.

In Chicago, boomers tend to buy up multimillion-dollar condos and

single-family houses in the city, preferably near the ballet, opera, and

theaters, says luxury real estate broker Sheldon Salnick.

Five years ago, rich suburbanites aged 50 to 70 made up only about 5%

of his clientele at Dream Town Realty. Now it’s about 10% to 15%, he

says.

What they want

New buildings now offer amenities tailored to this demographic,

Salnick says. They include concierge services similar to those offered

at hotels. Such services make it easy to arrange for dog walkers, plan

parties, or bring in a masseuse after a stressful day on the golf

course.

“They’re coming from 5,000- to 6,000-square-foot houses. They want

space. They want an office. They want room for their [visiting] kids,”

Salnick says. “They’re interested in things being done for them.”

To cater to these “booming” buyers, urban builders are now putting up

more two-bedroom residences with dens and expanded “laundry rooms,”

which are generally repurposed into hobby or craft centers or miniature

home offices, says Isabell Kerins, a director of product and business development at Irvine, CA–based John Burns Real Estate Consulting.

She’s also seeing more elevators installed, even in residences with

just two floors. And builders are bringing back wet bars and showy wine

rooms, closets, and nooks, often with glass enclosures and

refrigeration, she says.

More services to meet their needs

In Philadelphia, graying new residents are already revitalizing the

historic city. More high-end dining, boutiques, and even pop-up shops

are catering to these new residents, says Harris Steinberg, executive director of the Lindy Institute for Urban Innovation at Drexel University.

Nationally, more mixed-use developments with housing, businesses, and

services such as doctor’s offices are expected to go up in urban areas,

says Jean Setzfand, senior vice president of programs

at AARP, a Washington, DC–based nonprofit and lobbying group for older

Americans. They will be aimed at both older and younger city dwellers

who don’t want to drive or hop in an Uber to pick up necessities, get a

checkup, or enjoy a night out.

More art galleries, theaters, and other cultural organizations are

also expected to sprout up to appeal to these patrons with ample

supplies of both leisure time and money.

And Setzfand expects cities will create more open, car-free, and park

spaces where residents of all ages can walk, bike, and enjoy

warm-weather concerts. It’s a trend already well underway in places like

New York.

“Older individuals are stronger voters,” Setzfand says. “That’s why a

lot of the local leaders are paying attention” to what they want. And

they’re working to change cities to meet those needs.

But these perks come at a familiar price: gentrification. In the

oldest parts of Philadelphia, for example, boomers are driving up rental

and sale prices, which is in turn driving out some of the younger and

existing residents who don’t have such deep pockets, says the Lindy

Institute’s Steinberg.

More urban suburbs

Those in the Washington, DC, area who aren’t ready to cut the

suburban cord often move to closer-in, walkable suburbs that are more

like small cities themselves, like Bethesda or Chevy Chase, MD, says

real estate agent Asmeret Demeter-Medhane. There’s an influx of condos going up in these areas a stone’s throw from great restaurants and shopping.

Those buyers, like other urban dwellers, are seeking more amenities

says Demeter-Medhane, of Long and Foster Real Estate at Christie’s

International. And they’re willing to pay for it—to the tune of $700,000

and up.

She’s seeing more buildings come online that appeal to older buyers

with their “massive” master bedrooms, huge kitchens, libraries, and

fireplaces in their units as well as 24-hour concierges and high-end

spas and fitness centers in their buildings.

“Ten or 15 years ago, everyone was moving out into the suburbs,”

says Demeter-Medhane, who estimates that about a quarter of her clients

are now boomers. “And now everyone is moving back in.”